Table of Contents

Introduction

Let’s be honest—mortgage payments can feel like a mystery. You write that check every month (or set up auto-pay), but do you really know where your money goes? If you’re like most homeowners, you probably glance at your mortgage statement and focus on the bottom line. But here’s the thing: understanding what makes up that monthly payment isn’t just helpful—it’s essential.

Think about it this way: you wouldn’t buy a car without knowing what’s under the hood, right? Your mortgage works the same way. Every dollar you send to your lender gets divided up—some goes toward actually owning more of your home (that’s principal), some covers the cost of borrowing money (interest), and the rest? Well, that usually goes into an escrow account for things like property taxes and insurance. When you understand how this breakdown works, you can make smarter decisions about everything from refinancing to making extra payments. The mortgage payment breakdown guide digs deeper into these components and shows you exactly how each piece fits together.

Now, before we get into the nitty-gritty of your monthly payment, let’s talk about the bigger picture for a second. Your mortgage payment doesn’t exist in a vacuum—it’s connected to your overall financial health. Take your debt-to-income ratio, for example. This number tells lenders (and you) whether you can comfortably handle your mortgage alongside your other debts. Getting a handle on this ratio before you buy—or even after you’ve been paying for a while—helps you understand what you can truly afford. Tools like debt-to-income ratio calculators make this math pretty straightforward. And here’s something that might surprise you: compound interest doesn’t just work for your savings account. It’s also working against you with your mortgage, accumulating over the life of your loan. Understanding how this works (check out this guide on compound interest) can help you see why paying a little extra each month can save you thousands down the road.

Want to get really hands-on with your mortgage planning? This is where mortgage calculators become your best friend. Sure, your lender gave you numbers when you closed, but what if interest rates change? What if property taxes go up? Tools like the mortgage calculator with principal and interest and the mortgage payment calculator with taxes let you plug in different scenarios and see what happens to your monthly payment. Trust me—it’s eye-opening. You’ll start to see how even small changes in interest rates or tax assessments can impact your budget.

What You’ll Learn in This Guide

We’re going to break down everything you need to know about your monthly mortgage payment—no financial jargon, no confusing explanations. Just straight talk about how your money works. Here’s what we’ll cover:

- Mortgage Payment Components: We’ll explain exactly what principal, interest, and escrow mean for your wallet, and why understanding each piece helps you make better financial decisions throughout your homeownership journey.

- Calculation Methods: You’ll learn the math behind your monthly payment (don’t worry, it’s not as complicated as it sounds), including how loan amounts, interest rates, and terms all work together to determine what you pay.

- Reading Your Statement: Ever look at your mortgage statement and feel lost? We’ll show you how to read it like a pro, spot potential errors, and understand when escrow changes might affect your payment.

- Practical Tips: This is where the real value is—actionable strategies to manage your mortgage smarter, find refinancing opportunities that actually make sense, and use extra payments to cut years off your loan.

Throughout this guide, we’ll keep things practical and point you toward helpful resources like the mortgage loan process steps so you understand how everything connects. You’ll also discover why keeping tabs on things like mortgage refinance rates comparison can help you spot money-saving opportunities, and how knowing about mortgage payment grace periods can protect your credit score if life throws you a curveball.

By the time you finish reading, you’ll have the confidence to take control of your mortgage instead of just going through the motions each month. You’ll know exactly where your money goes, how to potentially reduce what you pay, and how to build equity faster. Ready to finally understand what’s behind that monthly payment and maybe save some money along the way? Let’s dive in and decode your mortgage payment once and for all.

Introduction

Your monthly mortgage payment might feel like this mysterious black hole where money disappears every month. But here’s the thing—when you actually know what you’re paying for, everything changes. Whether you’re already making those payments or you’re house-hunting and trying to figure out what you can afford, breaking down these costs gives you real power over your finances. You’ll be able to budget smarter, spot opportunities to save money, and maybe even sleep better knowing exactly where your hard-earned cash is going each month.

Breaking Down the Key Components of Your Mortgage Payment

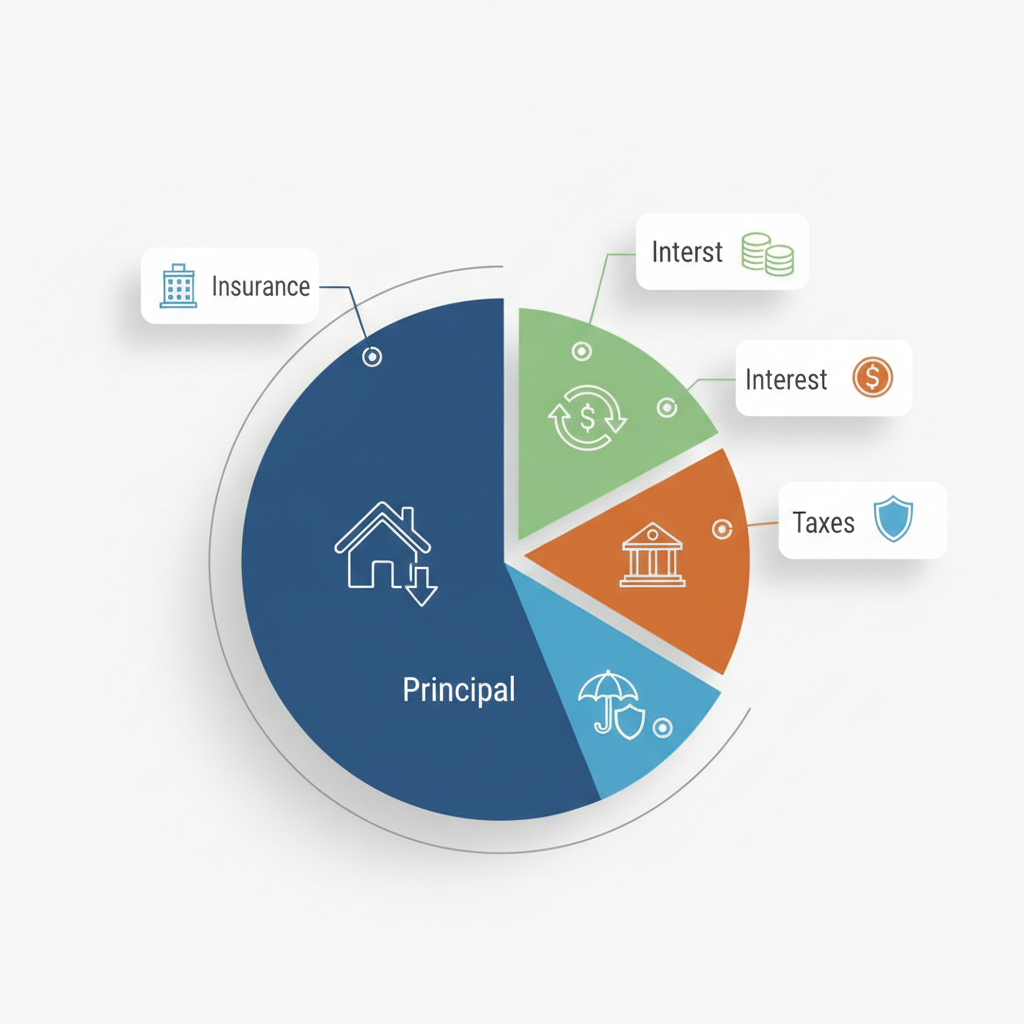

Think of your mortgage payment like a pizza cut into four main slices: principal, interest, taxes and insurance (held in escrow), and sometimes a few extra toppings like mortgage insurance or HOA fees. Each piece serves a different purpose in your homeownership journey. The principal? That’s the satisfying part—it’s actually paying down what you borrowed, chipping away at your debt month by month. Interest is what your lender charges for letting you borrow their money (hey, they’ve got to make a living too). For a really clear picture of how all these pieces fit together, check out this comprehensive mortgage payment breakdown guide that walks through each component step by step.

Now, here’s where it gets interesting. That escrow portion? Your lender is basically playing the role of your responsible friend who holds onto money for your property taxes and homeowner’s insurance. They collect it with your monthly payment and stash it away until those bills come due. Smart move, really—it protects both you and them by making sure these crucial payments never get missed. Sometimes you’ll also see mortgage insurance (if you put down less than 20%) or HOA dues rolled into this monthly amount. Just remember, when property taxes go up or your insurance premium changes, your payment can shift too. That’s why tools like the mortgage payment calculator with taxes are absolute lifesavers for planning your budget and avoiding those “wait, how much?” moments.

Key Elements You Should Know

Getting familiar with these components puts you in the driver’s seat of your mortgage:

- Principal: This is the real deal—the actual loan amount you’re paying off. Every month, a portion of your payment goes toward reducing what you owe. Here’s something cool: as your balance drops, so does the interest you’ll pay going forward. Early on, most of your payment goes to interest, but that flips over time.

- Interest: This is the price tag for borrowing money, and it depends on your interest rate and how long your loan runs. Got a fixed-rate loan? Your rate stays the same. Adjustable-rate mortgage (ARM)? Buckle up—that rate can change, and so can your monthly payment.

- Escrow for Taxes and Insurance: Your lender becomes your personal savings account manager here, collecting money for property taxes and homeowner’s insurance. When those bills arrive, they’ve got you covered. Just know that if tax rates or insurance costs change, this part of your payment will too.

- Additional Fees: Depending on your loan and where you live, you might see mortgage insurance or HOA dues bundled in. These aren’t always permanent—mortgage insurance often goes away once you’ve built enough equity.

Once you’ve got these basics down, you’re ready to make smarter moves. Whether that’s considering refinancing, planning extra payments, or just budgeting more effectively—knowledge is your best tool for homeownership success.

Calculating Your Mortgage Payment and Smart Management Tips

Want to know the secret behind those monthly payment numbers? It all comes down to three key factors: how much you borrowed, your interest rate, and how long you have to pay it back. These work together through something called an amortization schedule (fancy term, simple concept) to determine your fixed monthly payment for principal and interest. Then your lender adds the estimated taxes and insurance on top. The cool thing is, once you understand this formula, you can see exactly how different scenarios play out. What if you make extra payments? What if rates drop? The mortgage calculator with principal and interest lets you test drive different options and see what makes sense for your situation.

But calculating payments is just the beginning—managing them well is where the real magic happens. Refinancing can be a game-changer if you time it right, potentially lowering your payment or shortening your loan term. The trick is staying on top of market rates and knowing when to make your move. Resources like mortgage refinance rates comparison guides can help you spot those opportunities. And here’s a pro tip: even small extra payments toward your principal can save you thousands in interest over the life of your loan. It’s like compound interest, but working in your favor. Don’t forget to review your escrow account annually either—property taxes and insurance premiums change, and you want to make sure you’re not overpaying (or underpaying and facing a surprise bill later).

Effective Mortgage Payment Management Strategies

Ready to take control? Here are some proven strategies that actually work:

- Refinancing Options: Keep an eye on interest rates and don’t be afraid to crunch the numbers. Sometimes refinancing can slash your monthly payment or help you pay off your loan years earlier. The key is weighing the costs against the benefits for your specific situation.

- Extra Principal Payments: Even an extra $50 or $100 toward principal each month can make a huge difference over time. You’re essentially buying yourself out of future interest payments—and who doesn’t want that kind of return on investment?

- Review Escrow Accounts: Once a year, give your escrow statement a good look. Make sure the property tax and insurance amounts match reality. If something seems off, call your lender. It’s better to catch these things early than deal with payment surprises later.

- Stay Informed on Mortgage Rates: You don’t need to check rates daily, but keeping a pulse on trends helps you make smart timing decisions. When rates drop significantly below what you’re paying, that’s your cue to start exploring refinancing options.

Here’s the thing about mortgage payments—they’re not as complicated as they seem once you break them down. Your monthly payment has three main parts: principal (which chips away at what you owe), interest (the bank’s cut for lending you money), and escrow (your safety net for property taxes and insurance). Think of it like this: early on, most of your payment feeds the interest monster. But as time goes on? More money starts attacking your actual loan balance. It’s pretty satisfying to watch that shift happen.

Now, calculating what you’ll actually pay each month comes down to three big factors: how much you’re borrowing, your interest rate, and how long you want to take paying it back. These work together to set your fixed payment for principal and interest, plus whatever goes into escrow. And here’s something that trips up a lot of people—your mortgage statement isn’t trying to confuse you. It’s actually showing you exactly where every dollar goes. Once you know how to read it, you can budget better and catch mistakes before they become problems. Want to get ahead of the game? Consider refinancing when rates drop, throw extra money at your principal, or keep an eye on your escrow account. These moves can save you serious cash and help you build equity faster.

Ready to put this knowledge to work? Start with some reliable mortgage calculators online to crunch your numbers and play around with different scenarios. Getting familiar with the mortgage loan process steps will keep you confident through every stage of home financing—no surprises, just informed decisions. If you’re feeling ambitious, check out strategies to pay off your mortgage early and kiss those interest payments goodbye sooner. When rates look good, diving into mortgage refinancing and using our mortgage refinance rates comparison guide could put real money back in your pocket. And don’t forget—having an emergency fund is like having insurance for your insurance. Learn how to build one with our guide on how to build an emergency fund.

You’ve got the knowledge now. You understand how your payments work, where your money goes, and what moves you can make to optimize everything. That’s powerful stuff. The difference between homeowners who struggle and those who thrive? They take action on what they know. So stay on top of your mortgage, don’t hesitate to ask experts when you need help, and remember—every smart decision you make today builds a stronger financial tomorrow. Your home isn’t just where you live; it’s one of your biggest investments. Time to make it work for you.

Frequently Asked Questions

-

What happens if I miss a mortgage payment?

- Missing a mortgage payment typically results in late fees and can negatively affect your credit score. It’s important to contact your lender promptly to discuss options and avoid further penalties.

-

Can I change the escrow portion of my mortgage payment?

- Yes, but only if your property taxes or insurance premiums change. You’ll need to contact your lender to adjust the escrow portion accordingly.

-

How much of my payment goes to interest vs. principal?

- Early mortgage payments primarily go toward interest, while over time, more of your payment is applied to the principal, reducing your loan balance.

-

Is it beneficial to make extra mortgage payments?

- Yes, making extra payments toward the principal can reduce the total interest paid and shorten the length of your loan, saving money in the long run.

-

Can property taxes increase my mortgage payment?

- Yes, if your property taxes increase, your escrow payments will rise, which will increase your overall mortgage payment.